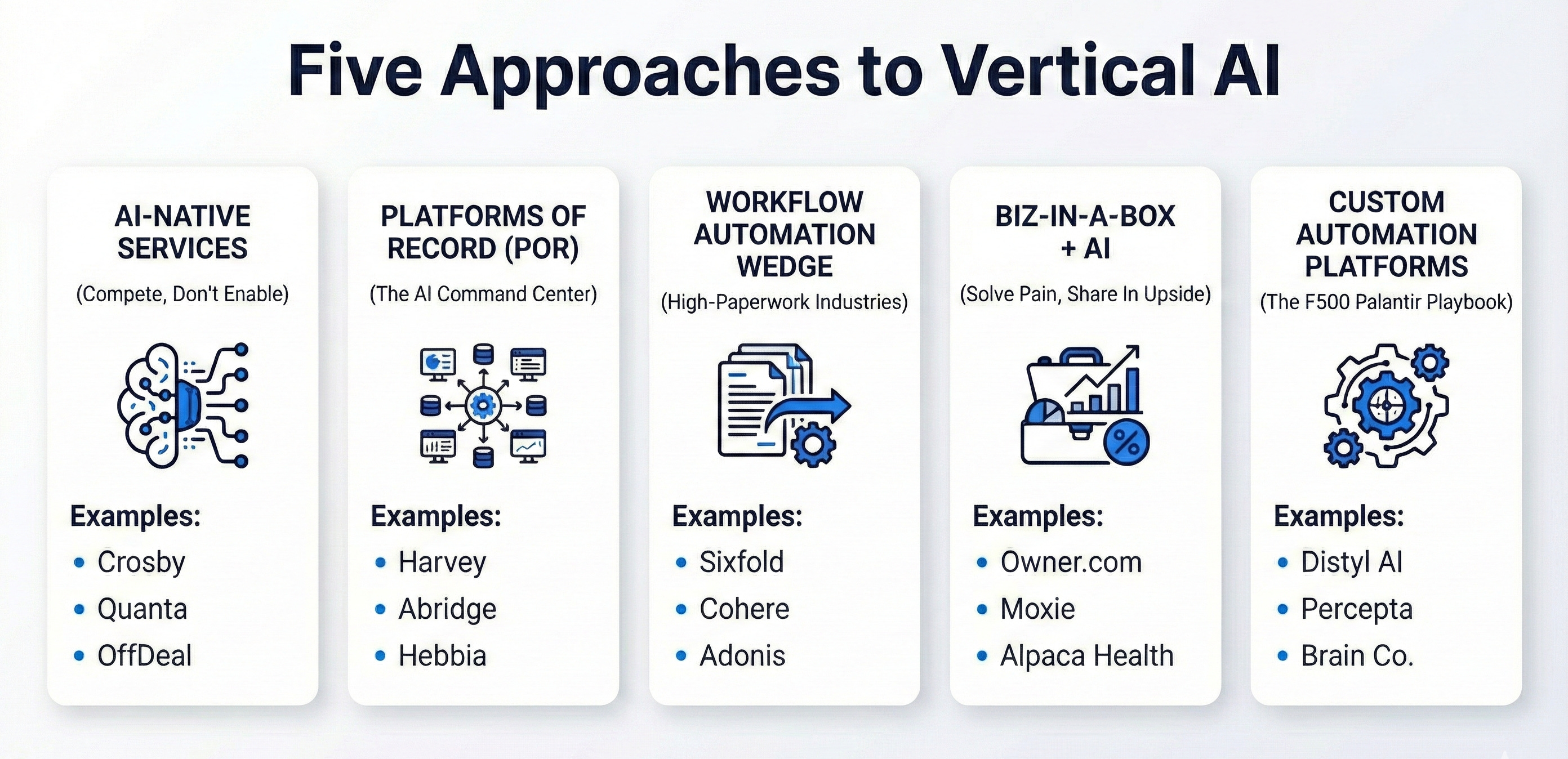

Five Approaches to Vertical AI

Capital Efficient #11

Welcome to the latest edition of Capital Efficient. Let’s get into it.

Five Approaches to Vertical AI

Something is breaking in vertical software - and how to respond to it is top of mind for founders and investors alike. SaaS multiples have compressed to roughly 3x. AI-native startups face margin pressure from inference costs that didn't exist in the prior era. And AI can now work autonomously across multi-hour tasks - capabilities that open up entirely new ways to build businesses, not just new ways to build software.

These shifts are unlocking business models for vertical AI that look very different from the last generation of venture-backed startups. A year ago, vertical AI meant one thing: sell high-ACV software to an industry that hadn’t been digitized yet. That playbook is still alive, but it’s no longer the whole story. The best founders I’m talking to aren’t just asking “what’s the best vertical AI platform to build?” - they’re asking a harder question: “given everything AI can do right now, what’s the highest-leverage way to build a business in my industry?” This is my attempt to map the five distinct approaches I see working in 2026 - and where I think each one goes from here.

1. AI-Native Services: Compete, Don’t Enable

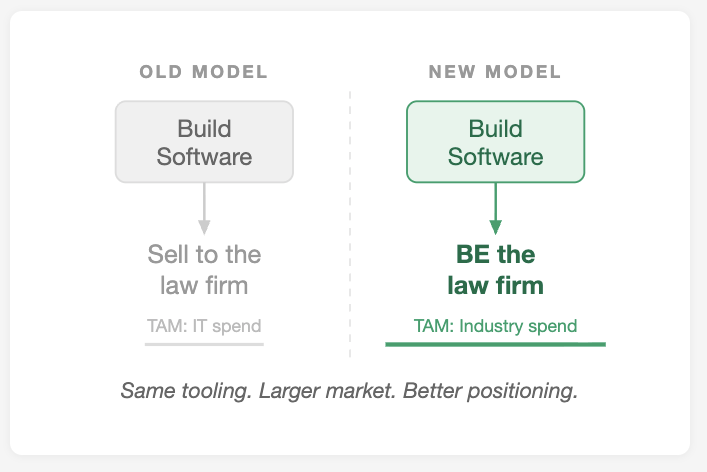

The traditional vertical software playbook was straightforward: enable an industry to digitize by selling it category-specific SaaS. But as AI gains the ability to take real-world actions, startups can now compete directly within an industry, not just sell software to it. An AI-native law firm goes after legal spend, not IT spend within law firms. An AI-native accounting firm is the accountant, not the software vendor for bookkeepers. The addressable market for competing is dramatically larger than for enabling, and AI allows new entrants to operate with margins approaching software-level economics while capturing revenue streams previously off-limits to technology companies.

My logic: vertical AI platforms are betting enterprises will shift labor spend to software spend, justifying outsized ACVs. But that premise cuts both ways. If AI is genuinely powerful enough to automate at that scale (and command those ACVs), you should be able to use the same tooling to compete directly as a services business; but at margins that legacy incumbents can’t touch. And if AI stalls out and that automation promise doesn’t fully materialize, the high-ACV platforms flame out anyway, because their valuations were built on ACV assumptions that never arrived.

In a lot of verticals, competing directly might be the better bet. Same tooling, better positioning, without the dependency on your customers agreeing to spend record-setting amounts on software and a much larger end market. Some examples we are already seeing in this bucket:

Legal: Crosby is an AI-native law firm for startups backed by Index & Sequoia that has raised $25MM in the last year. On the other end of the spectrum, Norm Law is an AI-native Big Law competitor that has raised $140MM from Blackstone, Bain & Coatue.

Accounting: Quanta raised a $15MM Series A led by Accel and is going direct to startups as the accountant, rather than selling software to CPAs.

Insurance: Coverage is a Sequoia-backed AI-native insurance broker capturing margins with AI-driven efficiency, having raised ~$50MM. They offer businesses insurance policies directly vs. building SaaS for incumbents.

Investment Banking: OffDeal is an AI-native investment bank doing the deals, not selling deal-sourcing software, having raised $17MM led by Radical Ventures.

PR/Comms: Blazel is an AI-native content and PR platform drafting pitches, generating media lists, and monitoring coverage at startup-friendly pricing, having raised $7MM led by Sierra Ventures.

The playbook: take an expensive or inaccessible professional service, rebuild it with AI at the core, capture the full value of the efficiency gain rather than selling it to incumbents for a fraction.

Another way to think of this model is Tech-Enabled Services 2.0. We saw lots of startups raise in 2010-2020 for tech-enabled services bets but they largely failed due to brutal unit economics. AI changes that cost structure and makes this model worth revisiting. The key difference: back then, a legal tech startup still needed armies of paralegals and associates to deliver the work; today, a 20-person team can do what once required hundreds. AI-native services also has a more forgiving market structure - vertical software tends to cluster around one or two category winners (we will get to these), and the 10th-best platform is dead. But the 10th-biggest insurance wholesaler or law firm is still doing hundreds of millions in revenue.

2. Vertical AI Platforms of Record

Another way founders can win in Vertical AI is to build the Platform of Record for their industry. This is a more traditional venture bet - use AI to either replace a legacy vSaaS player or build an AI-native platform of record (POR) for an industry that hadn’t seen a venture-scale outcome. So what does this look like? Picture a High-ACV software platform designed for orchestrating agents and copilots. Every industry knows it needs to implement AI but most don’t know where to begin. By building a vertical AI platform of record, you can sell an easy-to-implement, compliant command center for driving AI automation within a category.

Examples of startups building vertical AI platforms of record include Harvey (legal, $5B valuation, $190MM+ ARR), Hebbia (finance/consulting), Abridge (healthcare, $550MM+ raised). Within Bowery’s portfolio, Harmonyze is building the platform of record for franchisors.

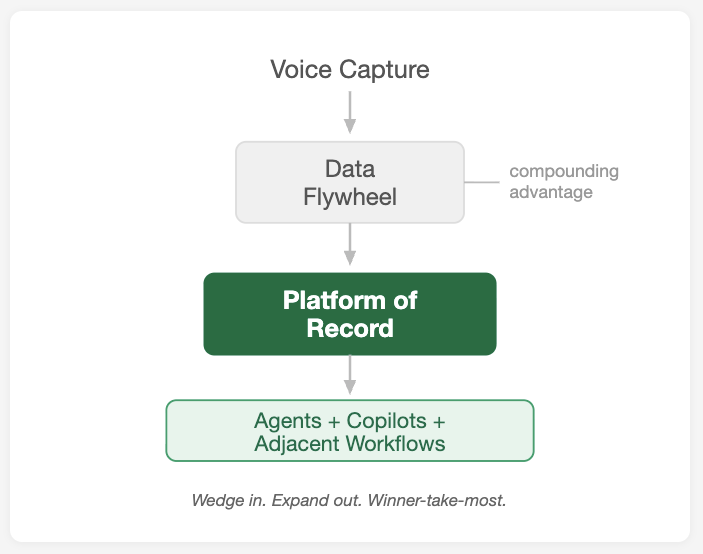

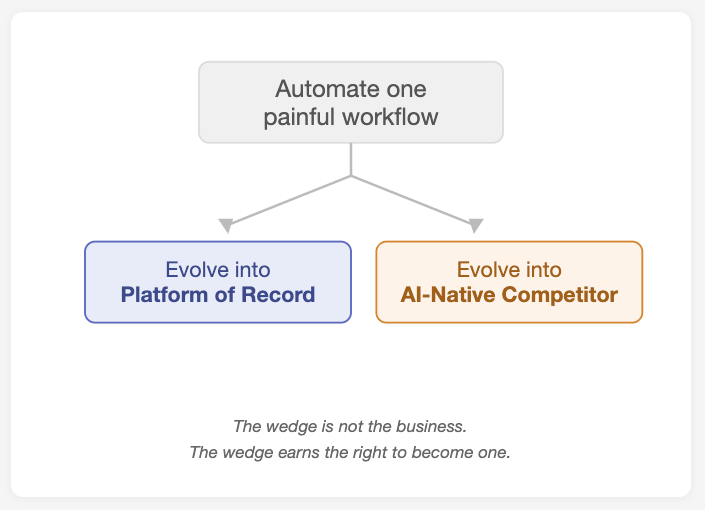

Voice as a wedge. One of the most effective entry points into building a POR is voice - especially in industries where workers aren't at desks. Field sellers, construction crews, home health aides, and technicians were largely bypassed by the last wave of cloud software. Voice meets them where they are.

Hospital Systems: Abridge used voice-first clinical documentation as its wedge into large health systems, then expanded into RCM and broader platform capabilities. Voice capture was the beachhead; the data flywheel is what made it a POR. Over $550MM raised, $2.75B valuation.

Home Healthcare: Roger Healthcare records in-home patient visits via voice and auto-fills the OASIS assessment, government-mandated Medicare documentation that takes clinicians 2-3 hours per patient. Home health aides are in patients’ living rooms, not at computers. Voice is the only interface that makes sense.

Field Sales: Bowery portco Enata is building the second brain for field sellers in categories like F&B, CPG, pharma, and med device. Reps brain-dump via voice throughout the day; Enata handles CRM inputs, follow-up emails, and ERP coordination, giving sellers back 2-3 hours daily.

In these categories, you’re often competing with no technology at all, so you don’t face the incumbent displacement problem that plagues most enterprise software. People share richer context by talking than by typing into a CRM. Whoever captures that voice data first in a given vertical creates a compounding advantage, and from there can earn the right to become the POR.

The risk: vertical software markets cluster around one or two winners, and many obvious verticals already have semi-entrenched leaders with massive war chests. For later entrants, the question is whether you can find a wedge, like voice, that provides a differentiated path before the window closes.

3. Workflow Automation

Vertical AI investors have poured money into two categories - healthcare and insurance - around the workflow automation opportunity. These are both industries that have lots of well-defined processes, a heavy paperwork burden, and clear rule-based guidelines for decision making. Digitizing high-volume, repetitive processes in industries that still default to fax, PDFs, phone calls, and spreadsheets is something AI can do right now with current capabilities, so it’s no surprise we’ve seen investor and founder interest in solving these challenges.

Healthcare: The most common targets for AI-native automation are prior auth and claims submissions. Prior auth is a massive, multi-step process involving payers, providers, and mountains of documentation still largely done by hand. The inefficiency has real consequences - delayed care, provider burnout, and billions in administrative waste annually. Companies like Adonis and Cohere have raised hundreds of millions solving prior auth bottlenecks.

Insurance: The $7 trillion insurance industry still runs on PDFs, Excel, and disconnected systems. The cost is real - slow underwriting cycles, missed submissions, and underwriters spending more time on data entry than risk judgment. The most common workflows being attacked by AI-native players are submissions intake and underwriting. Emerging players in this space include Sixfold and Further AI.

The best companies in this bucket won’t stay here. They’ll use workflow automation as a wedge to evolve into a Vertical AI Platform of Record or into an AI-native competitor using their workflow expertise and data advantage to compete directly with incumbents they initially served. The window for pure workflow automation as a standalone business may be closing as foundation models improve and horizontal tools handle simpler automation increasingly well. The companies that use their foothold to move up the value chain will build something durable.

4. Biz in a Box + AI

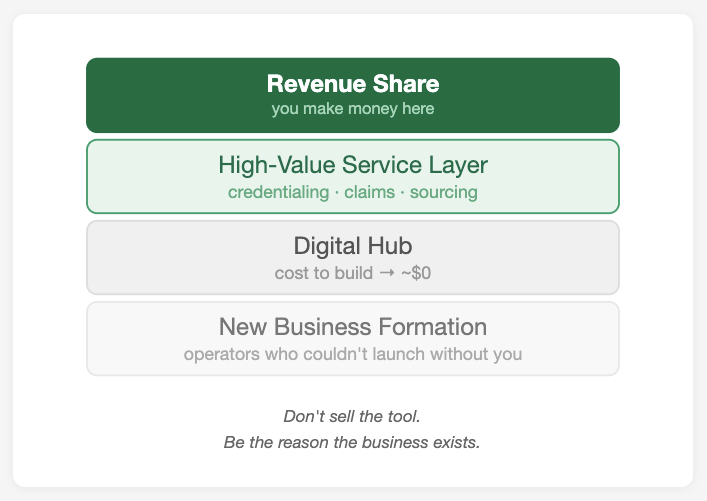

The last generation of vertical SaaS built for small businesses largely stalled out. Even the seeming winners of the 2015–2022 wave of biz-in-a-box software hit a ceiling at $10–20MM in revenue and never broke through - not because the products were bad, but because SMBs simply won’t pay meaningful ACVs for standalone software. The unit economics never worked. The vertical AI era makes this model worth revisiting. The new playbook flips the model: give small business operators a digital hub to run their operations, then monetize by owning a painful back-office task or a piece of their labor spend, taking a cut of revenue instead of charging a traditional software subscription.

One thing that’s exciting about this approach is these platforms don’t just serve existing SMBs; they enable new ones to form. Many aspiring operators never launch because barriers are too high: credentialing with payers, regulatory compliance, sourcing supplies at competitive prices. Platforms that solve these on Day One make first-time operators competitive with established players from the jump. Therapy is a canonical example. Alma and Headway recognized that independent therapists face brutal administrative overhead (credentialing, claims, billing, compliance), and that the back-office burden, not clinical skill, is the primary barrier to independent practice. Some examples of modern biz-in-a-box startups that are making it work:

ABA Therapy: Alpaca Health automates insurance onboarding, claims processing, and reimbursement optimization for ABA therapy providers serving children with autism, taking ~5% of topline. It removes a critical barrier to entry for new providers and wins when the provider wins.

Restaurants: Owner.com gives independent restaurants the digital stack that chains like Domino’s spent billions building: AI-powered websites, online ordering, SEO, and marketing automation - plus “AI Executives” that handle marketing, finance, and ops tasks. A first-time pizzeria owner gets access to the same conversion and reordering infrastructure as a national chain.

MedSpa: Moxie provides biz-in-a-box for MedSpas with better pricing on injectables, supplies, and equipment via collective purchasing power. A first-time operator gets Day One access to pricing that would normally take years of scale to negotiate.

The formula: provide the business-in-a-box (cost of building this now nearing zero), layer on a high-value service like credentialing, claims, sourcing, or better input pricing, and take a percentage of revenue. The best platforms won’t just be tools. They’ll be the reason new businesses get off the ground in the first place. Closely related to AI-Native Services (#1): the common thread is that AI can now do work, so you monetize the output, not the tool.

5. Custom Automation Platforms

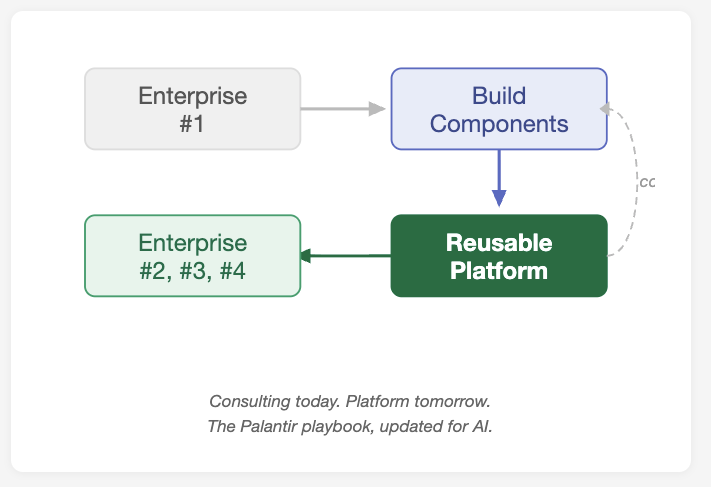

Every Fortune 500 company is strategizing around how to implement AI - to cut costs, drive growth, and maintain competitive edge. But for the very largest enterprises, most vertical AI startups are not broad enough or malleable enough to slot into their idiosyncratic workflows. These organizations have decades of calcified processes, complex technical architecture, and requirements no off-the-shelf product satisfies. Historically, when these businesses couldn't find software to automate something, their alternative was hiring consultants to build internal tools. The products those engagements produce are rarely best-in-class, and they don't compound. Now a third path is emerging: Custom Automation Platforms (CAPs).

Distyl AI - Founded 2022, raised $175MM at a $1.8B valuation in a September 2025 Series B led by Khosla Ventures and Lightspeed. Its Distillery platform deploys AI agents directly into Fortune 500 workflows across healthcare, telecom, and manufacturing.

Percepta - Incubated by General Catalyst, launched publicly in October 2025 with no disclosed investment amount. Deploys engineers directly inside enterprises via its Mosaic platform, with clients including Fortune 500 companies and state governments.

Brain Co. - Founded 2024, raised a $30MM Series A led by Elad Gil and Jared Kushner’s Affinity Partners. Bridges Silicon Valley AI talent with large enterprises and governments via a strategic partnership with OpenAI.

What makes CAPs distinct is their heavy forward-deployed model: they start by doing unscalable things for individual enterprises, but each engagement builds reusable automation components for a proprietary technical platform. Distyl calls theirs Distillery. Percepta calls theirs Mosaic. All three are trying to use bespoke deployment to build a core asset that compounds, then scale it across lookalike customers. The key open question for the category is who builds and maintains these workflows in the long run: the CAP's forward-deployed engineers, or the customer's own teams? The answer determines whether this model scales like a software business or plateaus like a services one.

The playbook: custom, n-of-1 automations. Charge implementation plus ongoing maintenance. Each engagement builds reusable components for a core technical asset, following the Palantir playbook. Automate claims for a top-five payer, then go to the other four with a speed advantage. Right now this looks like consulting. The bet is it evolves into something with real technical leverage and software-like scalability. One dynamic worth watching: Anthropic and OpenAI are hiring their own forward-deployed engineering teams to deploy into massive regulated organizations and drive token consumption, putting CAP startups in direct co-opetition with the model providers themselves.

These five buckets aren’t rigid categories. Companies move between them. The best workflow automation companies evolve into platforms of record or direct competitors. The best biz-in-a-box platforms are really AI-native services with outcome-based pricing. A Custom Automation Platform that builds enough reusable components starts to look like a vertical AI POR for the F250. The framework is less a taxonomy than a map of entry points, and the most interesting companies are the ones that use one bucket as a wedge into another. The question I’d ask any vertical AI founder right now: which of these five are you building for your industry, and why?

Deals

ElevenLabs raised a $500MM Series D at an $11B valuation in early February to cement its position as the default voice AI infrastructure layer. This came on the heels of news they had passed $300MM in ARR. Sequoia led, with a16z, ICONIQ, and Lightspeed all participating. If you’ve interacted with a synthetic voice in the last year, there’s a decent chance it was running on their models. The question at $11B is whether they stay an API business or push into end-user products - my bet is both, and the volume of voice interactions flowing through their platform gives them a data advantage that compounds over time.

GenLogs raised a $60MM Series B to build an AI-powered freight intelligence platform. The round was led by Battery Ventures with IVP, Cathay Innovation, Venrock, and Autotech Ventures participating. GenLogs operates a nationwide network of roadside sensors and satellites to give insurance firms, freight brokers, and government agencies real-time visibility into U.S. trucking - a dataset that simply didn’t exist before them. They’re already serving ~100 customers. The real moat here isn’t the software, it’s the compounding data asset: every sensor deployed and every mile tracked makes the intelligence layer harder to replicate and more valuable.

What I’m Reading

It was a banner week for X articles on vertical software - a few interesting ones:

10 Years Building Vertical Software: My Perspective on the Selloff (@nicbstme) After nearly $1T wiped from software stocks, founder Nicolas Bustamante argues LLMs are eroding vertical software’s premium moats — learned interfaces, custom business logic, bundling — while proprietary data, regulatory lock-in, and network effects survive. A moat redrawing, not a moat destruction.

Rebuttal to “10 Years Building Vertical Software” (@atelicinvest) The Unemployed Capital Allocator pushes back: the “AI kills software” narrative misunderstands what software actually is — accumulated domain knowledge delivered through a trusted relationship — and distribution moats, organizational inertia, and enterprise change complexity will protect incumbents far longer than the bears expect.

In Defense of Vertical Software (@gsivulka) Hebbia’s George Sivulka argues the value of enterprise software was never the code or interface — it’s “process engineering,” the deep understanding of how a specific team does their specific job — and that last-mile organizational knowledge, calcified over years of collaboration, is precisely what LLMs cannot commoditize.